Explain How Target Costing Differs From Traditional Cost Reduction Methods

To compete effectively organizations must continually redesign their. An organization will be profitable when the created value is greater than the costs of production and service supply.

Target Costing Key Features Advantages And Examples

The management can determine the desired profit margin.

. Under traditional cost reduction after market research to determine customer requirements and product specification engineers and designers. Under traditional cost reduction after market research to determine customer requirements and product specification engineers and designers determine product design then the cost to produce the product. Features of Target Costing.

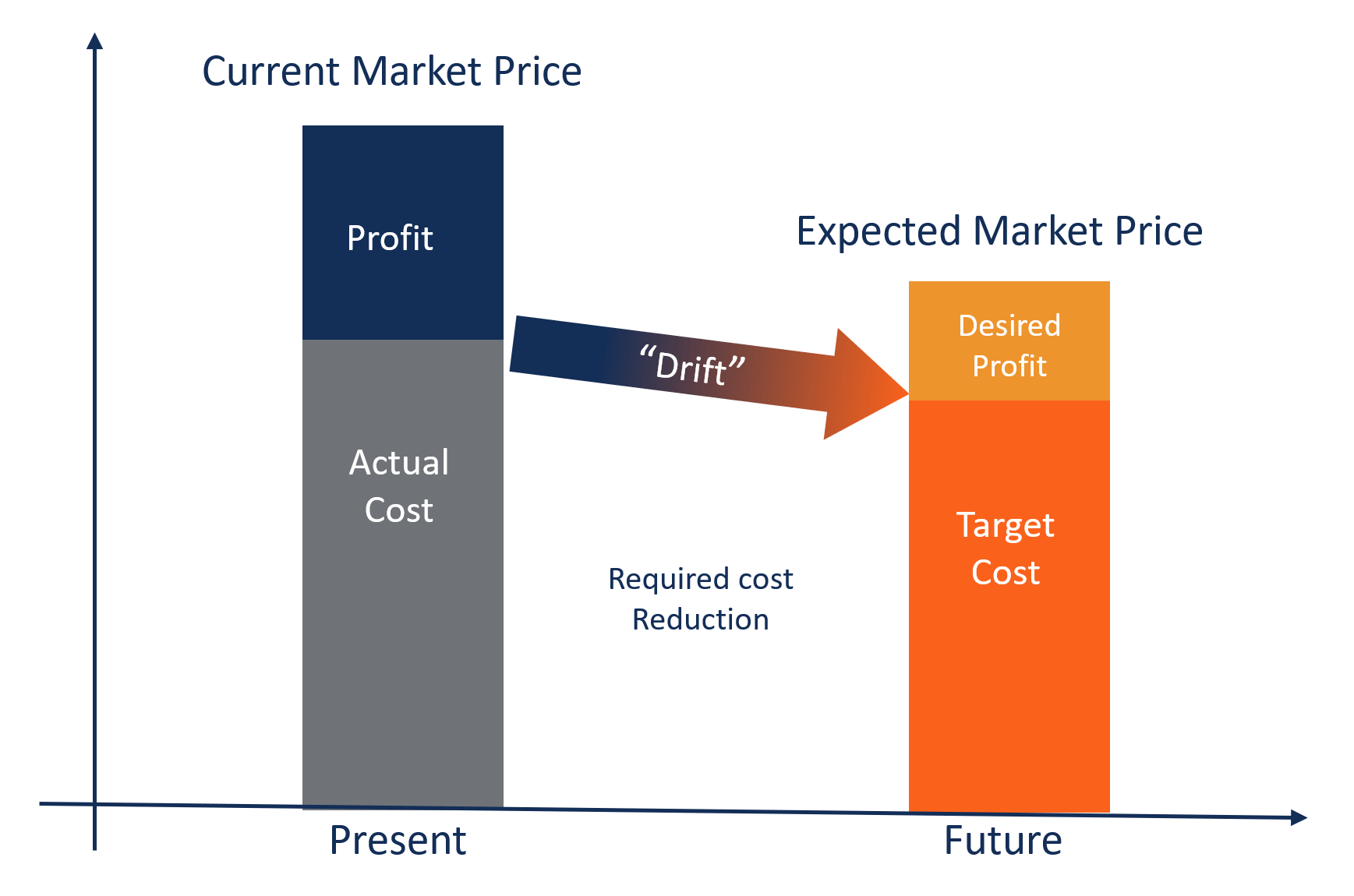

Target costing is the method which company sets the production cost by deducting profit margin from the target selling price. Target cost means an estimation of total cost to win in the competition in terms of quality cost and productivity. Explain how target costing differs from traditional cost reduction methods.

Under the target costing allowable product cost ie. Write an essay that. Costs for the product are then calculated and compared to the cost target mentioned above.

Students also viewed these Accounting questions Traditional cost reduction versus target costing Traditional cost reduction in the United. Objectives of target costing. It is not a method or technique of costing.

The total life cycle costing approach should therefore lead to more cost-effective products and services. Explain how the total-life-cycle costing approach differs from traditional product costing. It requires much more attention to the production life cycle.

Target Cost is the remaining balance after deducting profit from selling price. The purpose of target costing is to help a firm to remain and to compete in the market iii the long run. Traditional cost-based pricing is designed to appeal to any customers but target costing targets specific customers.

Students also viewed these Accounting questions Explain how target costing differs from traditional cost reduction methods. There are different methods of costing for different industries. Under traditional cost reduction after market research to determine customer requirements and product.

Disposal costs are most relevant when an organization has to eliminate any harmful effects associated with the end of a products life. Target Costing compared with the traditional method of cost management The difference between target costing and traditional method of cost management represented in Table 1. Explain how the conceptual framework is useful in situations where there is How does absorption costing differ from variable costing in cost accumulation and.

It is a part of management process. Then the desired profit margin is subtracted from the predicted target selling price to arrive. Target costs on the other hand are the difference between target prices paid by the potential customers and the reasonable profits.

In contrast target costing focuses on cost reduction at the RDE stage. But it is a management technique used to survive under the increasing competitive environment. Target costing versus traditional cost reduction methods According to this the target costing and traditional cost reduction methods approach the relationships among cost selling price and profit margin quite differently.

Company uses this strategy by setting the selling price determine desirable profit and calculate the target cost. The method of costing to be used in a particular concern depends upon the type of manufacturing and nature of industry. In the modern days fast growing industries use target costing approach moves the decision perspective from book keepers office to the market.

In the traditional cost-plus pricing method materials labor and overhead costs are measured and a desired profit is added to determine the selling priceTarget costing involves setting a target cost by subtracting a desired profit margin from a competitive market price. Explain how target costing differs from traditional cost reduction methods. This gap would have to be closed by some form of cost reduction if.

Product cost is not important in product design under traditional cost-reduction methods which focus on cost reduction at the manufacturing stage. The methods or types of costing refer to the techniques and processes employed in the ascertainment of costs. If a target-costing system is used and the existing cost cannot be reduced to the target cost through cost reductions management should not produce and sell the.

This approach is to seek the lower costs by designing a quality product that reduces costs in the production phase. If the estimated cost is too high then it may be. Target costing focuses on achieving the target cost.

The traditional method standard costing is not effective in longer period for cost reduction. The target cost is the difference between the target selling price and target profit margin. Target costing is better suited to assembly-oriented businesses such as car manufacturing.

Basically there are two methods of costing. The difference between the current cost and the target cost is the cost reduction which management wants to achieve. The level of cost reduction was estimated as the difference between current and target cost.

The main features of target costing are presented below. Target costing also called product costing method in which an attempt at the planning and development phase of a product life cycle to attain a specified cost that is decided by management. Target costing differs from traditional cost reduction methods through the process by which costs are determined.

Target costing is criticized for its complexity and rigidity. The primary difference between target costing and traditional cost-based pricing is a. Explain zero-based budgeting and how it differs from the traditional approach to preparing next years budget.

Target cost is derived by conducting market research and predict the target selling price which is willing to pay for the product with specific characteristics. If it appears that this cost cannot be achieved then the difference shortfall is called a cost gap. Explain how four-variance analysis differs from one- two- and three-variance analysis.

In order to remove the drawback of traditional method the New Method of Costing is introduced. Traditional costing is better suited to process-oriented businesses that use continuous production. Traditional cost-based pricing considers the market that is available for the product at the end of the process whereas target costing considers the market at the.

734 Target costing differs from traditional cost reduction methods through the process by which costs are determined. The objectives of target costing are-Decreasing the costs to ensure the required profit level of new products. Explain how target costing differs from traditional cost reduction methods.

Meeting the set standards of the market for new products in terms of price delivery time and quality levels. 8-25 Target costing differs from traditional cost reduction methods through the process by which costs are determined. A team is formed to integrate activities such as designing purchasing manufacturing marketing etc to find and.

2

Target Costing Key Features Advantages And Examples

2

Comments

Post a Comment